PODCAST: Trust and National Security: What Being American Means at Home and Abroad, with Ambassador Joe Westphal and former FBI Executive Lauren Anderson Season 2 · Ep 44

0:00

1659

PODCAST: Trust and National Security: What Being American Means at Home and Abroad, with Ambassador Joe Westphal and former FBI Executive Lauren Anderson Season 2 · Ep 44

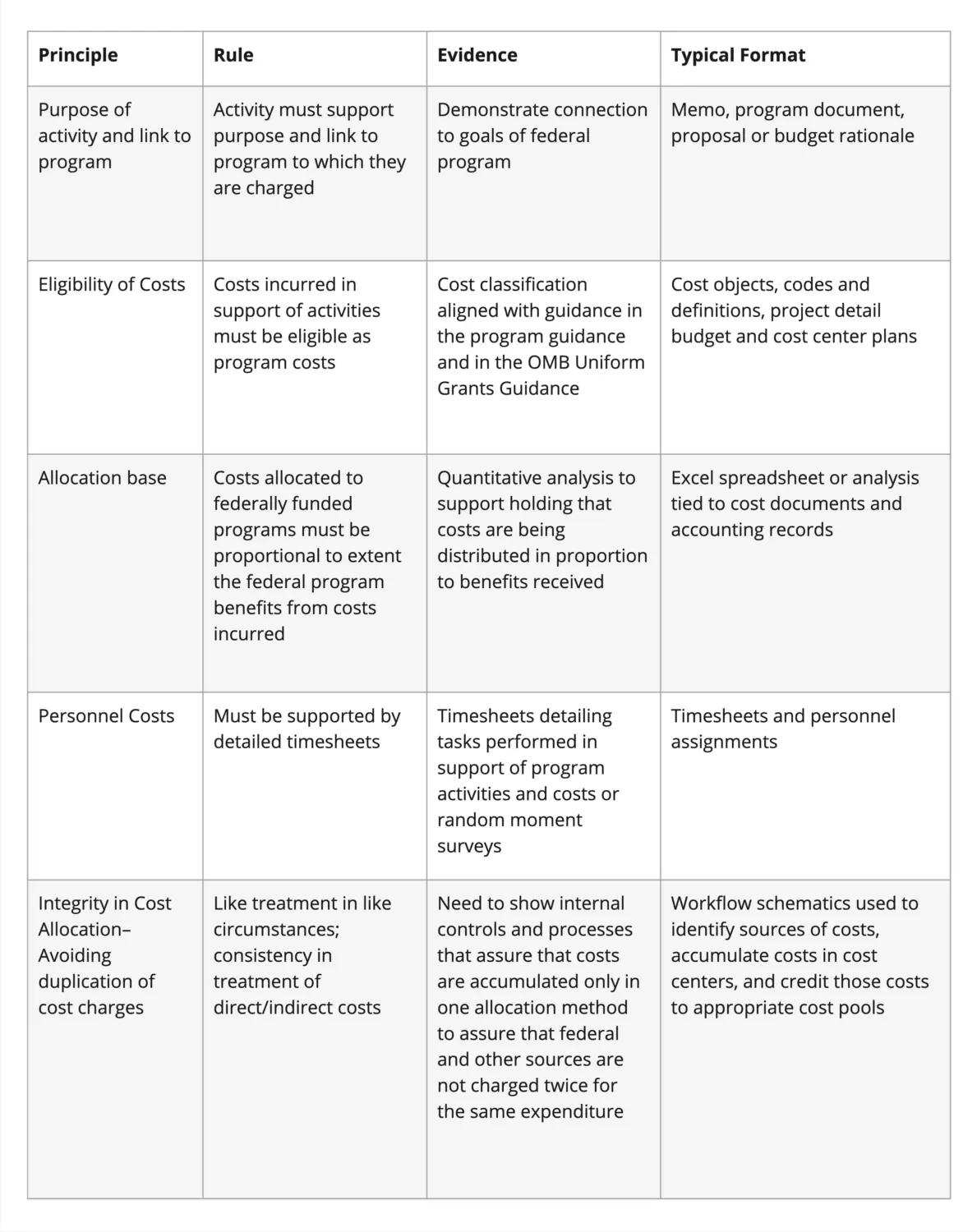

Any recipient (states, tribes, territories, local governments, non-profits) of more than $1,000,000 annually in federal funds is required to undergo a “single audit.” State-level auditors or other independent non-federal auditors “stand in” for the federal government in examining how grants and other expenditures are accounted for in the single audit using instructions in the most recent Compliance Supplement issued by OMB. As part of the single audit, the auditor looks at specific federal awards to see if the grantee is in compliance with the terms and conditions of the award for the specific program(s).

As part of this work, an auditor may examine the agency cost allocation plan to assess whether it is systematic and rational and to assure that costs are eligible for reimbursement and allocated appropriately. They will also examine the documentation used to determine the cost allocation methodology.

To justify its cost allocation plan and methodology, a jurisdiction should document decisions made about accounting treatment and keep them available in a folder or central repository.

In addition, it can acquaint the external audit team with plans for accounting for a major IDS project by:

Jurisdictions should make certain that the audit team is consulting the most recent versions of the Uniform Grants Guidance and the Compliance Supplement or other program guidance or waivers, and is aware of how clarifications and reference or technical guides provide further direction on the eligibility of costs for reimbursement from federal grants. They should consult early and often with the audit team about their plans, and familiarize the team with the treatment being proposed.

The key risk for IDS expenditures charged as direct costs to grants is whether the costs are eligible for funding under the federal grant in question. While the updated OMB Grants Guidance provides broad clarification that data and evaluation costs – including the costs associated with building an IDS – are allowable under federal financial assistance, it is important to confirm that each specific participating program does not have a unique limitation or other requirements for such costs. Auditors will want to review the federal grant descriptions of eligible costs and documentation showing that the system investments support those expenditures.

The auditor reviewing an agency indirect cost plan will be assessing the risk that all and only those indirect cost expenditures that are eligible for federal funding have been included in the agency indirect cost rate. They will also be focused on whether the cost allocation methodology is systematic and rational, distributing costs on an equitable basis to federal and other agency programs. To assess this, they will look for documentation that the indirect costs are eligible under the federally funded programs to which they are being charged, in line with the guidance provided in the Compliance Supplement for those programs.

Since the Statewide Cost Allocation Plan or Local Government Cost Allocation Plan has been reviewed and approved by the cognizant federal agency, the auditor will be focused on whether the underlying accounting transactions are consistent with the approved plan. This means that they will be focused on the accounting entries and cost accumulators used to identify costs and distribute to the appropriate indirect cost pools included in the SWCAP plan.

We use cookies to improve your experience on our site. By continuing to use this site, you accept our use of cookies. Privacy Policy

{kind=link}