PODCAST: Trust and National Security: What Being American Means at Home and Abroad, with Ambassador Joe Westphal and former FBI Executive Lauren Anderson Season 2 · Ep 44

0:00

1659

PODCAST: Trust and National Security: What Being American Means at Home and Abroad, with Ambassador Joe Westphal and former FBI Executive Lauren Anderson Season 2 · Ep 44

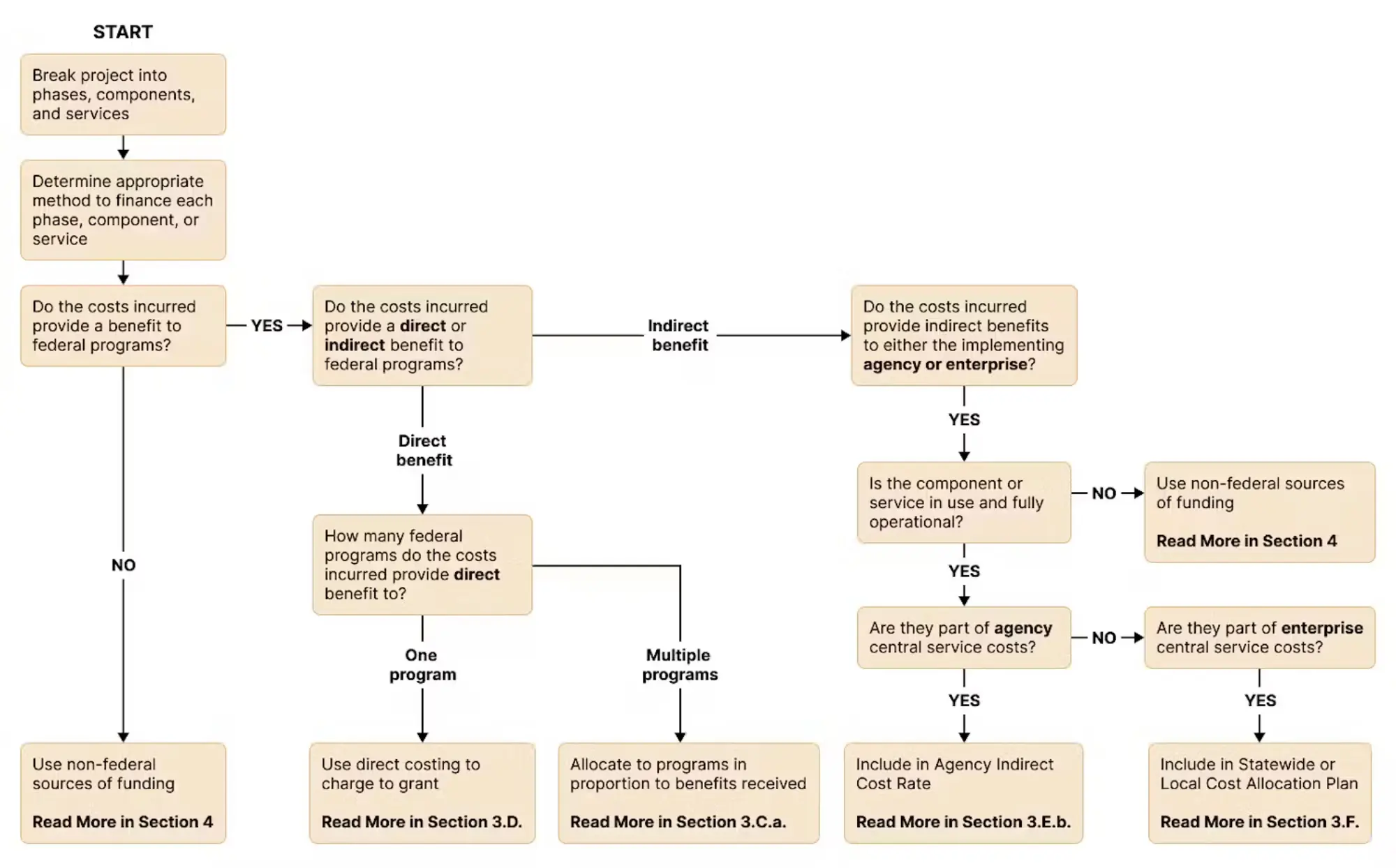

Paying for an IDS often involves multiple sources of funding that may vary during different phases of development, such as planning and design versus operating and maintaining the system. This section focuses on the different ways of using federal funds to pay for part or all of an integrated data system.

Whether your jurisdiction is just beginning to consider an integrated data system or has long experience, planning for how to sustain your IDS is important. This guide provides a roadmap and basic understanding of the information needed. Importantly, a successful planning process should include input from multiple stakeholders and support a collaborative approach to governance, system design, and identifying future intended uses.

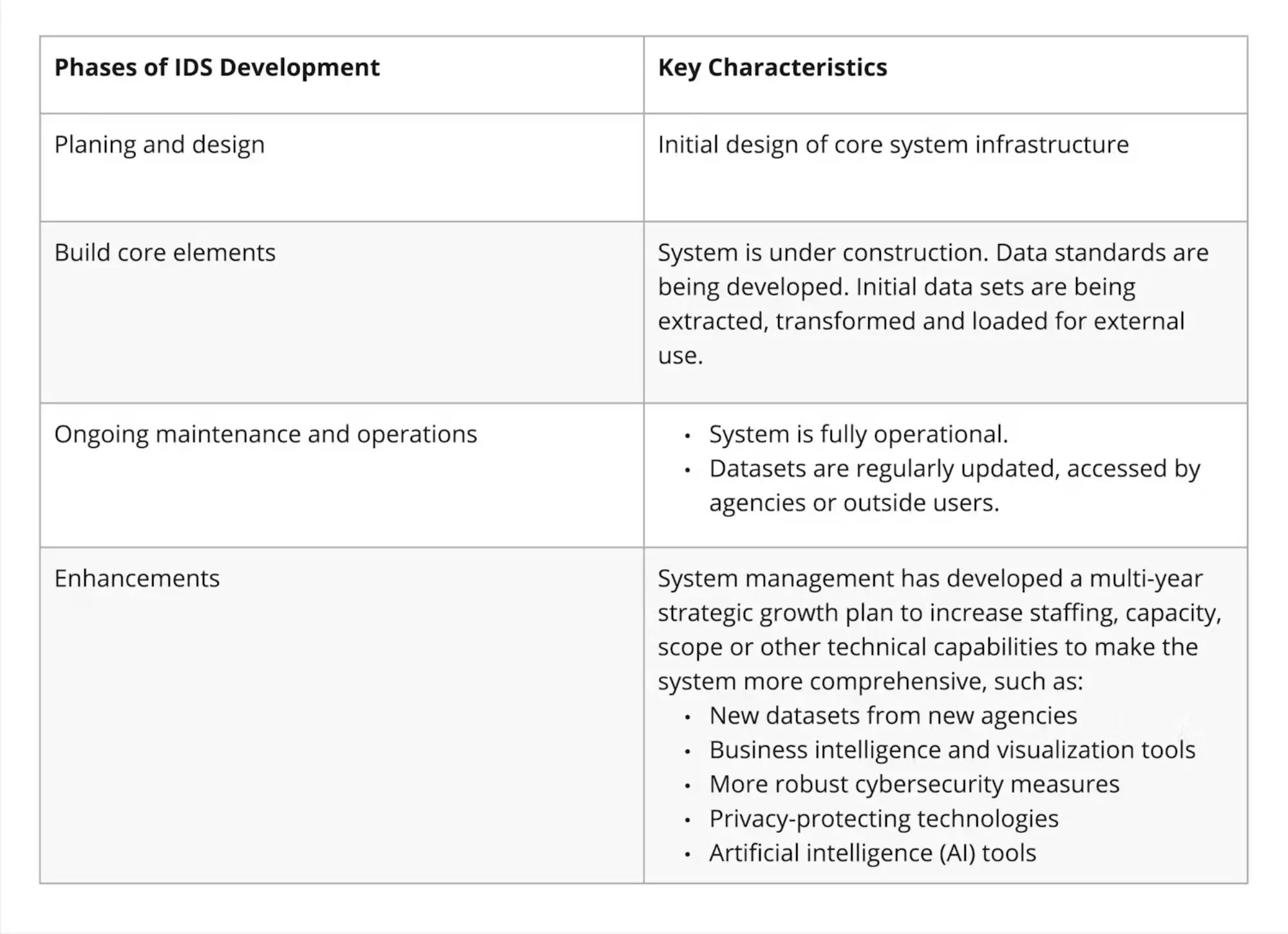

Two key concepts in financing IDS are phases of development and program alignment.

Program alignment describes how an integrated data system can benefit a single program by providing data from multiple sources. To the extent that your integrated data system is aligned with federal programs – meaning that programs get specific benefits from the system – the tools described in this field guide will help you to use federal funding to support the IDS.

What does program alignment look like in action? Read the field guide case study on how Ohio’s IDS supported better decisions across multiple programs.

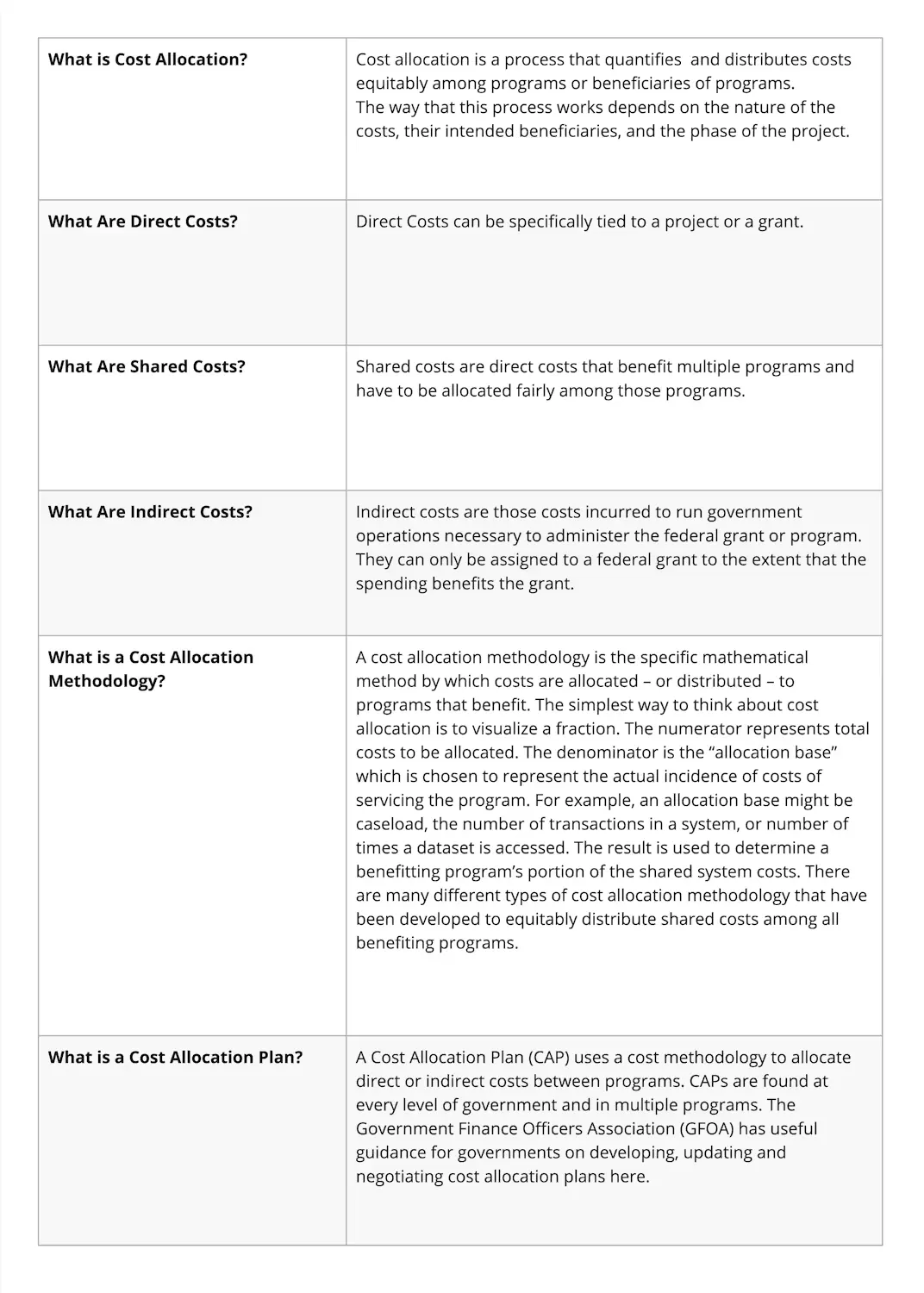

There is no single ¨right way¨ to finance all systems. Many, if not all, projects will likely use a number of different financing methods across stages of the system´s maturity. A key concept in selecting the right financing methods for your purpose is cost allocation, or the process of deciding which programs should pay for which costs.

Hear Katy Collins, Chief Analytics Officer in the Allegheny County Department of Human Services, explain how cost allocation supports staffing and financing for the county’s IDS and analytic capacity.

Cost allocation is a method by which costs for IDS are assigned to a number of different programs or beneficiaries, based upon how the IDS benefits them. In the case of integrated data systems, many programs combine administrative data from multiple program systems to achieve a number of program objectives such as program evaluation, continuous improvement, and program integrity.

For example, the IDS might produce analyses that help to:

These insights may be useful to either a single program or multiple programs. This distinction is important because it will help to identify direct costs, shared costs, and indirect costs, which are explained below. The type of cost will guide how you pay for it using federal funds. Regardless of type, this process of assigning costs to specific grants is done using a cost allocation methodology, as described below. The cost allocation methodology is used to produce a cost allocation plan (CAP). CAPs exist at all levels of government, both for specific programs and at the enterprise level.

Regardless of type, this process of assigning costs to specific grants is done using a cost allocation methodology, as described below. The cost allocation methodology is used to produce a cost allocation plan (CAP). CAPs exist at all levels of government, both for specific programs and at the enterprise level.

Direct costs can be specifically tied to a project or a grant, such as when a functionality, operation or analysis performed by the IDS benefits specific Federal programs. It is often the best way to get the core components or “base” of an integrated data system funded as the system is being built.

OMB’s updated Uniform Grants Guidance and the associated reference guides give examples of costs related to data and evaluation that may be classified as direct costs – and even address integrated data systems specifically. When using direct costing, getting multiple agencies or programs to co-invest can help lead to a sustainable system with broader-based governance, funding, and stakeholder support.

What can co-investment across multiple federal grants look like in practice? Read the field guide case study on how the U.S. Departments of Health and Human Services and of Agriculture worked with states to develop a toolkit.

Here are examples of how direct costing may work on a tactical level:

Indirect costs are incurred to run the Federal funding recipient’s operations. As a result, indirect costs benefit multiple programs and can’t be readily assigned to a specific program or activity. However, they may be allocated to specific federal grants to the extent that they benefit that particular grant. Examples of indirect costs can include procurement, human resources, cybersecurity, internal audit, finance, and IT networks. In addition, OMB’s revised Uniform Grants Guidance clarifies that costs associated with building integrated data systems for purposes of research, management, and evaluation are allowable as indirect costs, in addition to direct costs.

There are three ways in which a state, local, tribal, or territorial government or agency might get some or all of these costs reimbursed:

The method chosen to recoup these costs can help to generate the resources needed to invest and reinvest in common management functions to effectively and efficiently manage federal grants. Indirect cost allocation plans are easier to execute in a highly controlled, centralized governance structure. Where government operates in a fairly loose, decentralized manner, indirect cost allocation plans may be quite difficult to execute. In one city, each agency has negotiated its own federal indirect cost rate for those federal grants it handles most often. Other, smaller cities may opt for the simplified 15% de minimis indirect cost rate. To learn more about these approaches, see the full field guide.

How can a cost allocation plan help sustain robust integrated data in real life? See the field guide case study on how the City and County of Denver implements a cost allocation plan across a highly federated metropolitan area.

How can a cost allocation plan help sustain robust integrated data in real life? Read the field guide case study on how the City and County of Denver implements a cost allocation plan across a highly federated metropolitan area.

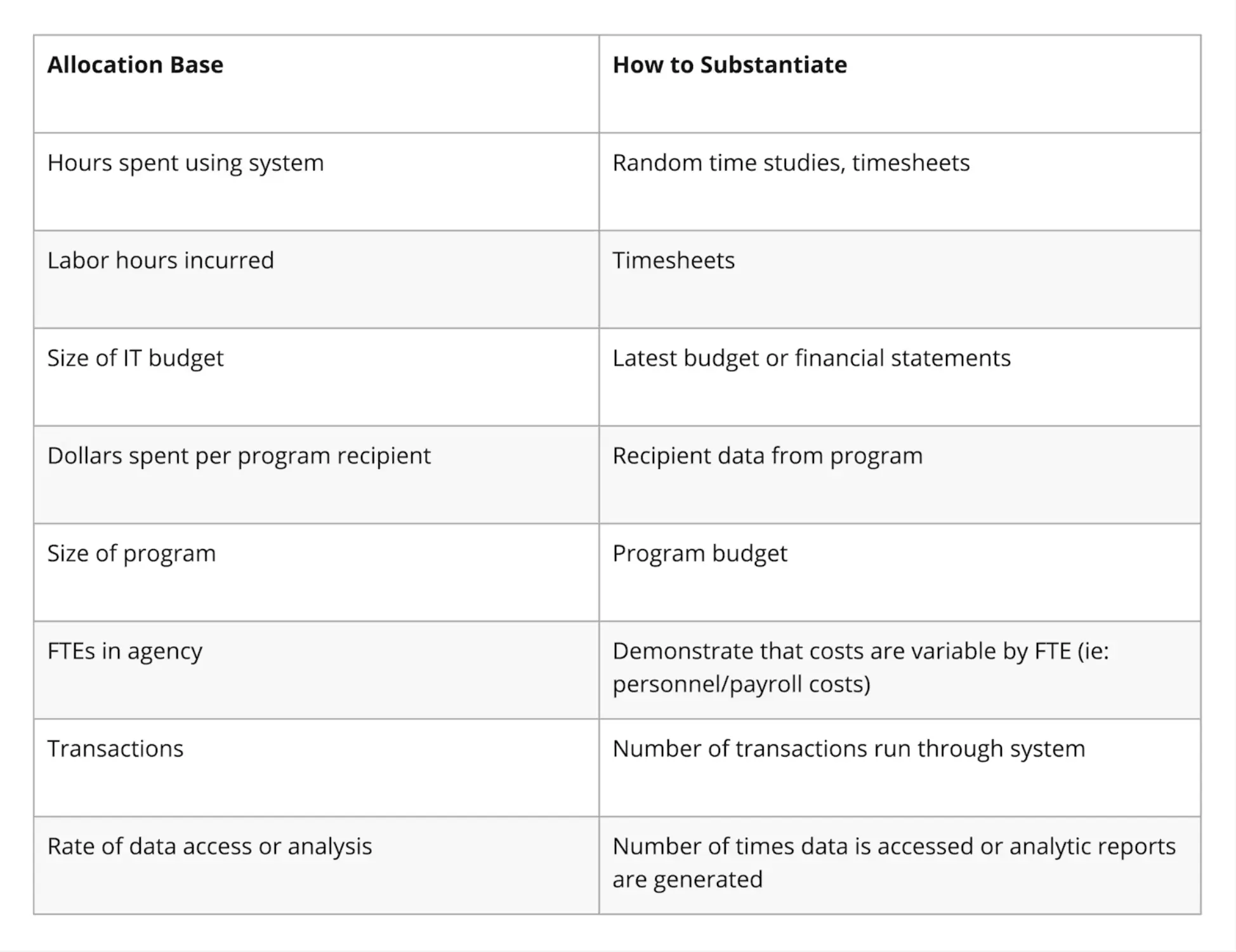

A cost allocation plan collects and allocates the total indirect costs of centrally provided services and allocates them to grants to obtain an equitable reimbursement for those costs. A vast number of possible allocation bases can be used, and they can vary across different cost pools, agencies, and programs. Some examples of bases used for allocation of IDS indirect expenses might include:

States and localities provide many enterprise-wide services that are funded through indirect costing. Many states choose to fund these services using a Statewide Cost Allocation Plan (SWCAP), or a Local Government Cost Allocation Plan at the local level. While traditional examples of enterprise services include human resources, legal counsel, and budget, OMB’s updated Uniform Grants Guidance clarifies that costs associated with data and evaluation are allowable indirect costs also.

SWCAP can be a particularly important financing tool for long-term maintenance and operation of integrated data systems that provide and support data and evaluation activities, such as for reporting, performance management, research, and evaluation. A government using this method of funding must be able to show that the integrated data system is (1) fully operational, and (2) benefits the government enterprise as a whole.

What does this enterprise-wide approach look like in practice? See the field guide case study on how Ohio uses SWCAP to support its statewide integrated data and analytics capacity.

What does this enterprise-wide approach look like in practice? Read the field guide case study on how Ohio uses SWCAP to support its statewide integrated data and analytics capacity.

We use cookies to improve your experience on our site. By continuing to use this site, you accept our use of cookies. Privacy Policy